One of the recurring themes of this newsletter has been the doom facing Great Britain, its economy and its undead empire, most recently rebranded as “Global Britain.” My curiosity about all this was prompted by the hysterical reactions from the U.K. to the U.S. withdrawal from Afghanistan in August 2021. A number of high-level British officials were indignant, as though they felt betrayed by the Americans. Who knew that Afghanistan was that important to the UK’s ruling establishment?

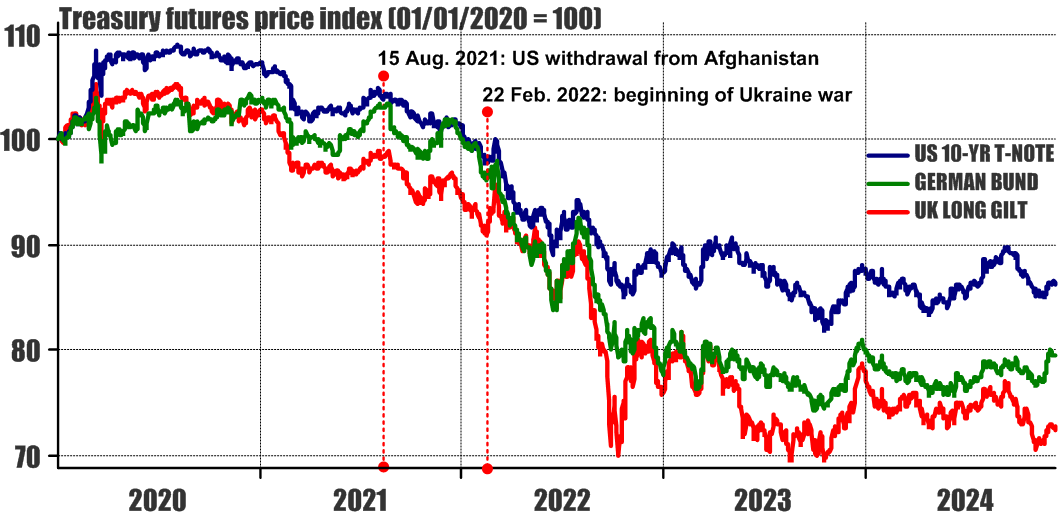

Further research revealed that Britain’s foreign policy entailed the continuity of an imperialistic, neo-colonialist agenda and that Britain was highly dependent on the United States for the attainment of her geopolitical objectives. U.S. withdrawal from Afghanistan triggered an almost immediate impact in the financial markets, which was further exacerbated by the breakout of war in Ukraine (you know, Russia’s unprovoked and illegal invasion of an independent democratic Ukraine):

Very soon, it became apparent that markets singled out the UK as the weak link among Western economies, suggesting that her economy was more exposed to West’s gradual loss of global hegemony and that the UK is likely to be one of the first - if not THE first of Western dominoes to fall.

In my October 2021 article, "The Fall of Global Britain: an Investment Hypothesis," I suggested that Britain "won't revert to simply minding its own domestic affairs as a neutral island nation, and will endeavor to regain its lost hegemony to the bitter end." Insofar as this was determined by the UK’s oligarchic, imperialistic system of governance, it was predictable that,

"The UK will ... suffocate its domestic economic growth by imposing hard austerity at home while at the same time increasing military spending and foreign adventurism. Britain's public debt will continue to outpace its GDP growth and the government's budget deficits will be covered by Bank of England's monetary inflation. This recipe reliably leads to stagflation and possibly to hyperinflation."

This all might seem surprising as Great Britain has exercised great skill in deflecting attention away from itself and its economic problems, and keeping up the appearance of a wonderful liberal democracy, one of the wealthiest nations of the world, a leader of the free world and a stronghold of human rights. But as is often the case, what’s apparent on a nation’s façade does not correspond to its much darker realities.

When systems of governance fail, their collapse have tended to display a certain syndrome which allowed me to venture the following prediction about the unravelling of the British system:

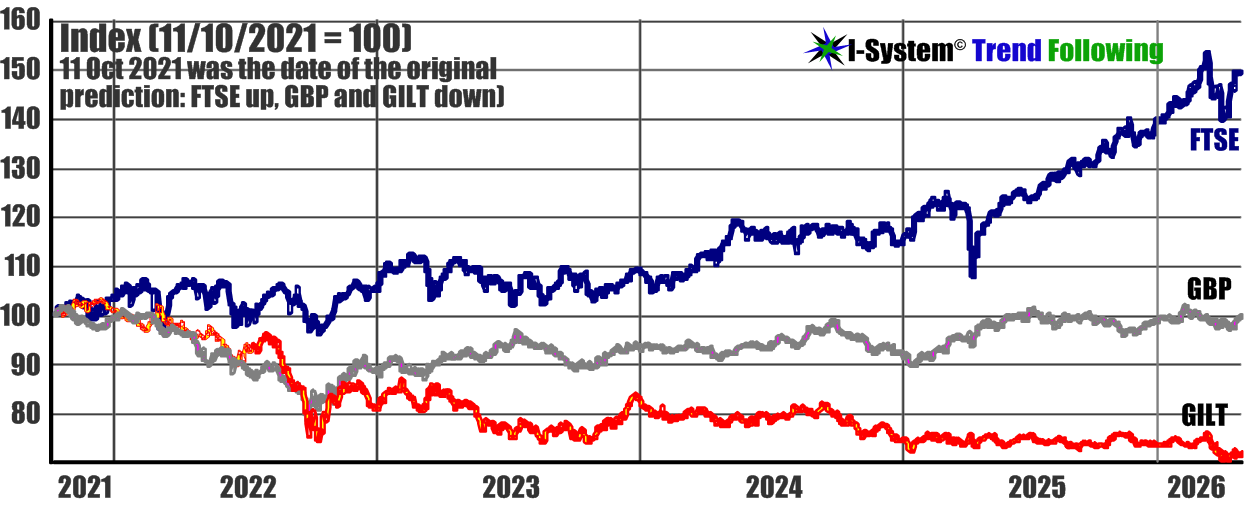

"... at a macro level, we can expect the following developments over the coming months and years: asset prices will probably continue to rise (i.e. a bullish cycle for the FTSE 100), but the government bonds will continue to slide along with the British pound."

I published this prediction on 11 October 2021. The following chart indexes British government bonds (gilts), British pound and FTSE 100 equity index:

With regards to gilts and FTSE 100, my prediction was correct. British pound, which has lost ground against the U.S. dollar through 2024 has recovered and is now almost exactly where it then was (1.3594 on 11 Oct. 2021 vs. 1.3527 at yesterday’s session’s close).

We have seen that geopolitical events preceded significant market events for Western economies and the same could prove true with regards to the ongoing events in the Middle East. This will become clearer with time but thus far, a number of items from the news cycle suggest that the deterioration of the British fiscal position and her economy recently accelerated.

For example, Britain’s economic prospects have been downgraded more than any other major economy in the International Monetary Fund’s (IMF) latest update on the state of the world. A brief SkyNEWS commentary about this is here.

📺 Sky 501 and YouTube 1:16 AM · Apr 15, 2026 · 3.08M Views915 Replies · 1.14K Reposts · 3.13K Likes

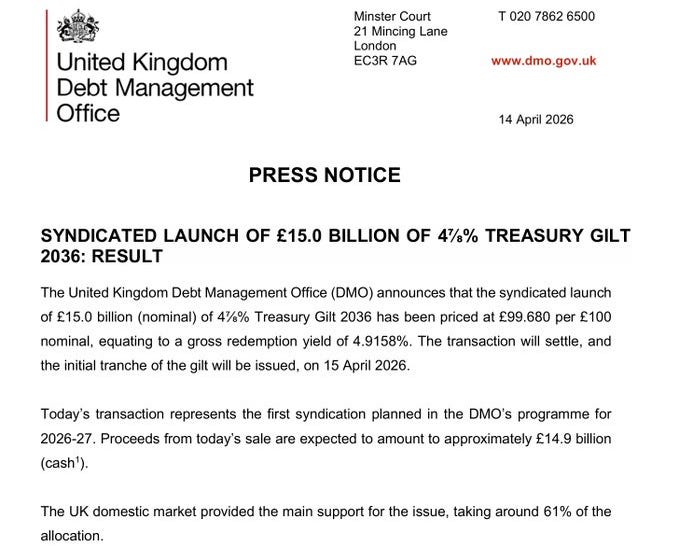

We also learned this week that the UK made the largest single gilt issuance in its history: £15 billion in a single day. What’s worse, it has done so at the highest yield in nearly twenty years.

Britain’s catastrophic fiscal position can also be seen from the fact that for the first time in her history, her welfare bill is now larger than its income tax revenues: £333 billion vs. £331 billion. In spite of this, the government seems undeterred, doubling down on its foreign adventurism as its ship sinks and life becomes unaffordable to millions of ordinary Britons. Clearly, Britain “won’t revert to simply minding its own domestic affairs as a neutral island nation, and will endeavor to regain its lost hegemony to the bitter end.”

I couldn’t explain why the British pound has held up so well over the past five years, but I still believe that my 2021 prediction will hold and that the pound will ultimately collapse along with the gilts. Equity prices will ultimately accelerate upward into a vertical climb for a simple reason.

UK monetary authorities have one tool left to manage this crisis. It is the printing press. As the Bank of England floods the system with liquidity, the people will lose confidence in their currency and will look to get rid of it as quickly as they can in favor of real assets (i.e. stocks). For this reason, the bulk of BOE’s accelerating quantitative easing will flow into the stock markets.

Unfortunately, the pound’s collapse will far outpace the nominal gains in stock prices, so the investors will still suffer devastating losses in real terms.

By Independent News Roundup

By Independent News Roundup