In Munich, she expressed doubts about European economy’s competitiveness and again warned about financial instability that lies ahead:

The ECB needs to be prepared for a more volatile environment. … We must avoid a situation where that stress triggers fire sales of euro-denominated securities in global funding markets…

Then on 18 February, only four days after that speech, the FT reported that Ms. Lagarde is planning to step down from the ECB, well before her term ends in October 2027. Who steps down early from such a privileged sinecure? Ms. Lagarde does not have grandchildren with whom she’d prefer to spend time. The obvious suspicion is that she knows that the “more volatile environment” may be coming quite soon and prefers to go while the going is good.

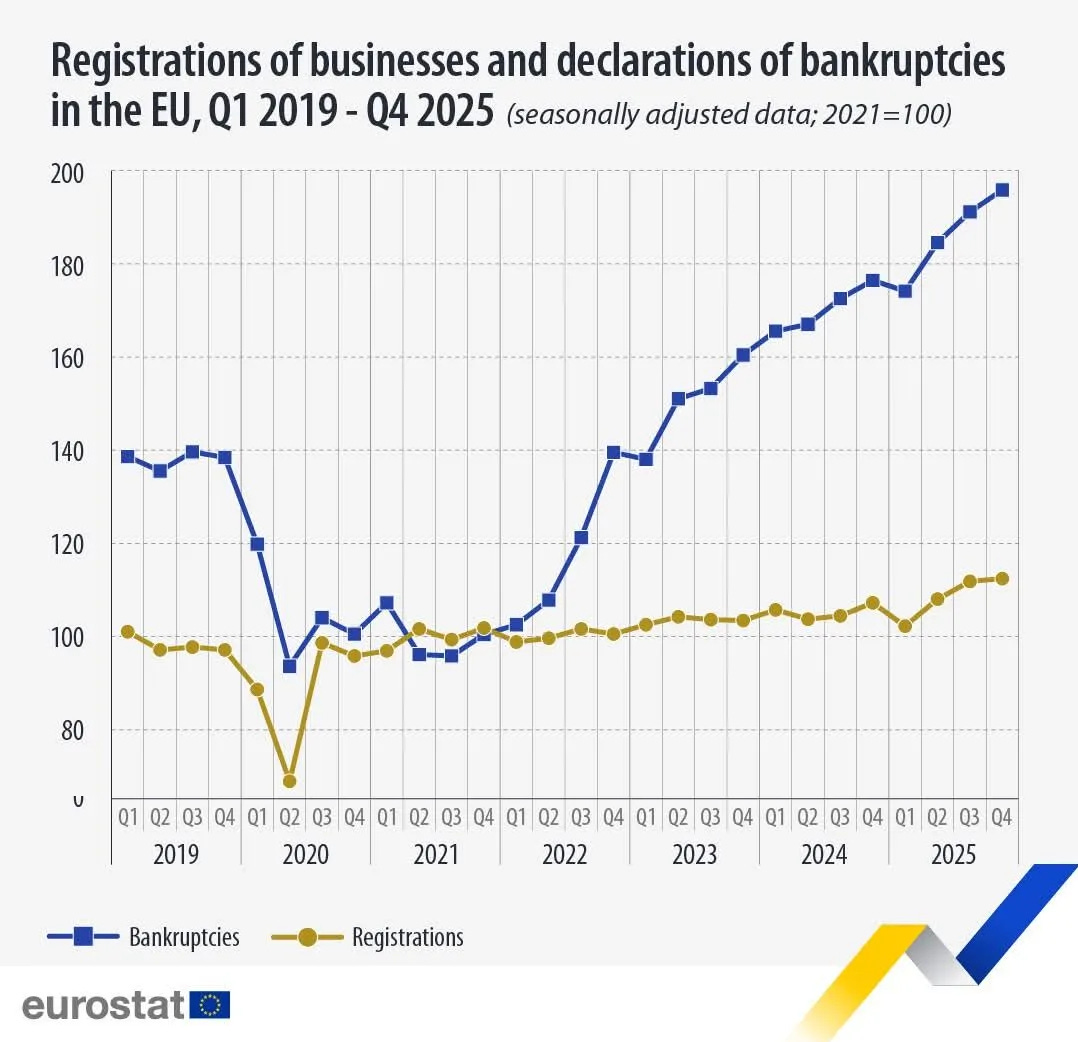

The fact that Europe’s economy is in a structural decline is not news. The following chart tells the story in two important aggregates: the number of companies going out of business vs. the number of new companies being formed:

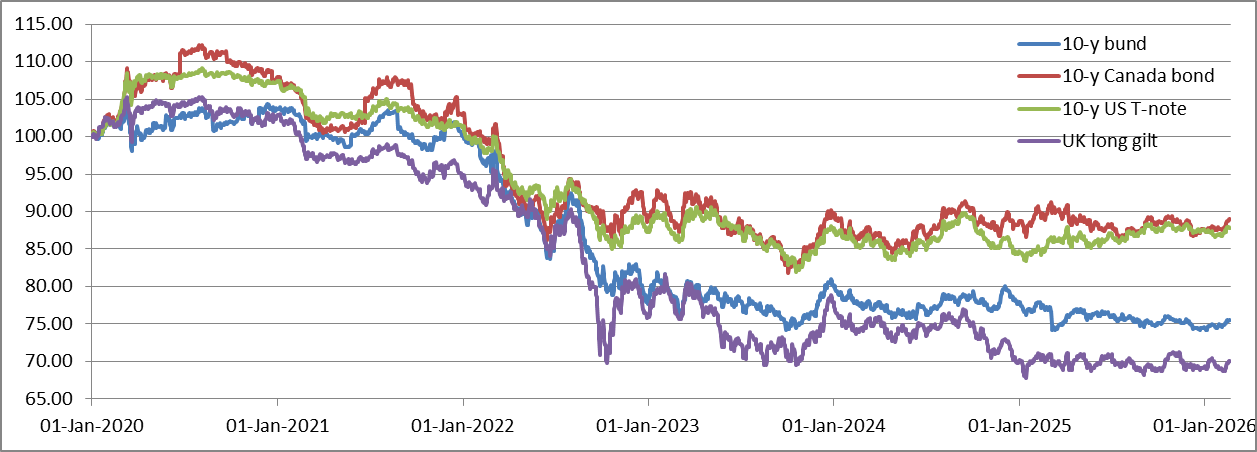

The trends are obviously quite dismal and only getting worse. While new business registrations are basically flatlining, bankruptcies are soaring. That’s Europe’s tax base falling off a cliff taking jobs along with it. And even if the markets aren’t registering these trends in the near term, it’s clear that on the longer horizon, the weakness of European economies is showing. The chart below shows the price of the U.S., Canada’s, Britain’s and Germany’s 10-year government bonds:

Again, we can see that the British debt is the weak link, but Germany is not doing much better. In this sense, Germany is something of a benchmark, since it’s still perceived as the safest European economy. Meanwhile, it’s interesting to note that the U.S. and resource rich Canada have clearly diverged from European economies, even if their performance has been merely flat. Given the dismal conditions in the bonds markets, flat may be the new bullish.

By Independent News Roundup

By Independent News Roundup