Following on from yesterday’s discussion, Mario Nawfal pointed out during our interview on Wednesday that crude oil prices were actually falling, suggesting the Middle East situation was under control and that commercial shipping would soon normalize. The markets were seemingly converging on that view. Namely, on Monday, 9 March, the Brent crude oil price spiked, reaching almost $120/bbl during the morning hours - more than $26/bbl above Friday’s $93/bbl close.

But from there it corrected sharply, falling below $83/bbl on Tuesday, which was more than $10 below Friday’s close. Of course, such volatile gyrations generate a lot of commentary and premature jumping to conclusions. What I tried to convey to Mario Nawfal and his audience was that we shouldn’t read too much into such short-term developments.

As readers of this newsletter know, large-scale price events (LSPEs) almost invariably unfold over intervals that can span months or even years. That’s the way this Iran episode will likely play out. In yesterday’s article I discussed the reasons why I believe that the current war might not conclude on the Trump administration’s desired schedule but on the basis of Iran’s strategic objectives, which could take months or years to accomplish.

This is why the Hormuz disruption could be long-lasting, and the markets will have plenty of time to digest it and react accordingly. Unfortunately for the rest of us, markets often overreact, implying that we could be in for unexpected surprises to the up-side. As the process unfolds, narratives will catch up to explain the price action and predict what happens next.

It has long been my contention that in securities markets, prices lead and narratives follow, as I summed up in this 2016 article: “Market facts vs. market narratives.” Once we are aware of this, we can see it happen again and again. In addition to the examples I discussed in the linked article, I highlighted another case in point with crude oil in 2023: as the price of a barrel rallied from the low $70s in June to the mid-$90s in September, analysts accompanied the move with a slew of reports and commentary explaining why this was happening.

On 23 September 2023, a ZeroHedge headline read, “US Shale Giant Agrees With JPMorgan: Oil Headed For $150“. The article laid out the market fundamentals that would propel the oil price toward JPMorgan’s target, but—surprise, surprise—that never happened. On the other hand, had the oil prices crashed, all the reports would be explaining the reasons why it crashed. The whole point of all that intellectual busywork is to forecast future price events, which is a total waste of time and effort.

Consider two articles that were published by Bloomberg, four days apart, in the summer 2022. Citi’s and JPMorgan’s learned analysts looked at the same market, did their homework and reached radically different conclusions:

Not to be forgotten, in 2020, the former next Warren Buffett, Cathie Wood made her own genius forecast that oil would go down to $12/bbl. That never happened either:

All these brainy narratives and predictions are duly reasoned by authoritative market analysts, who are armed with all the market intelligence that money can buy and always sound like they’re much smarter than you are.

It’s not disappointing that Ms. Wood got that secular forecast wrong. What’s disappointing is that she made the forecast in the first place. In the end however, some analyst will prove right in their forecasts and then they’ll probably be paraded in the financial press as “the analyst who predicted XYZ.. now they are saying that such and such will happen...” This kind of thing has been going on forever, but from an investor’s point of view, it’s all worth less than zero. It’s literally better to practice calligraphy than to listen to all the nonsense.

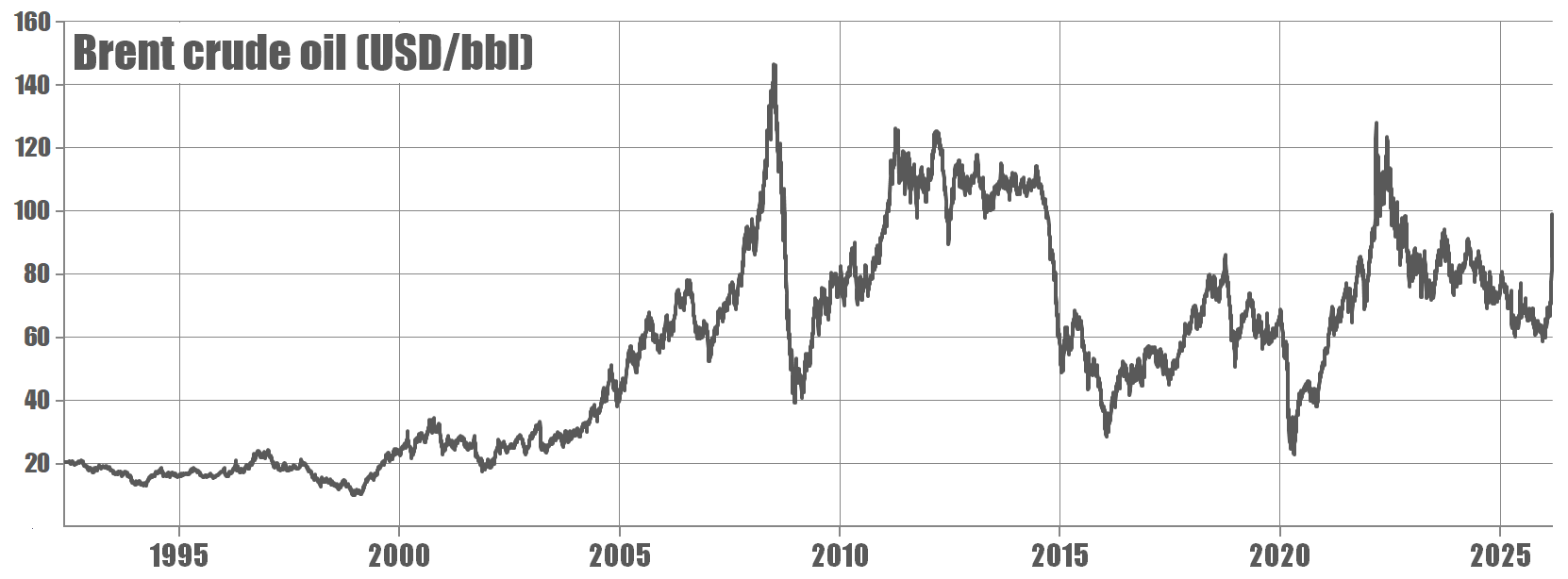

The indisputable fact about markets is that large-scale price events unfold as trends over months and years. Earlier this month we discussed how the price of gold languished for nearly three years in a horizontal range between $1,800 and $2,000 per troy ounce. Today it is trading above $5,000/tr.oz. That LSPE didn’t happen overnight; it spanned two years and it unfolded as a trend. We should expect the same process to unfold in energy markets. The long-term chart of oil prices is why I suspect that we ain’t seen nothing yet:

Today, a barrel of Brent crude trades at around $100 which, in view of the last 15 years of price action isn’t especially high, despite the fact that those 15 years never saw anything remotely similar to the Hormuz disruption that suddenly took about 20% of the world’s oil supply off the market and which might not normalize in the short term.

That suggests that the markets haven’t properly digested what just happened. They are like that Tomas and his family enjoying their lunch as an avalanche is barreling at them. The Hormuz disruption will almost inevitably drive the next LSPE to levels we have not seen before. Nobody could predict whether this might be $150, $380, or $500 per barrel, but we shouldn’t be surprised if the trend triggered by the war in the Middle East runs for many months. Unexpected surprises could be up ahead.

By Independent News Roundup

By Independent News Roundup